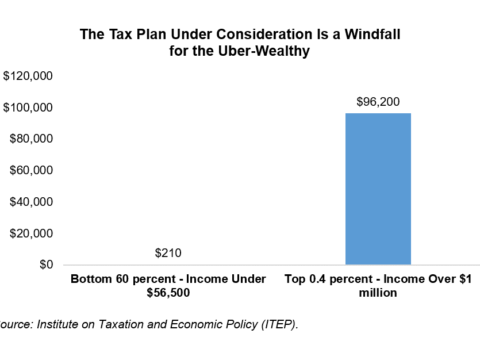

Federal Tax Cut Framework Is Designed for Millionaires

Under the tax framework released last week by the Trump administration and Congressional leaders, the wealthiest 1 percent of Kentuckians...

Kentucky Center for Economic Policy

Research That Works for Kentucky