A new federal Department of Labor (DOL) rule clears the way for states to offer a particular model of retirement plan for private sector workers without it being subject to...

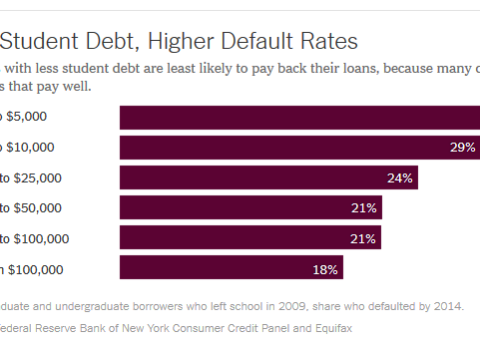

Data released today by the U.S. Department of Education shows Kentuckians leaving college with student loan debt are among the most likely to default nationwide. The state’s new default rate...

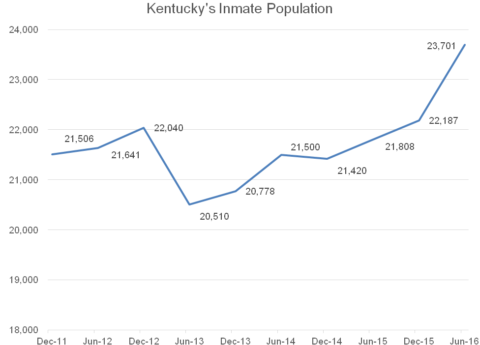

The impact of Kentucky’s 2011 criminal justice reforms on the state’s inmate population and budget have been much less than what was projected when Kentucky enacted HB 463, or the...

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok