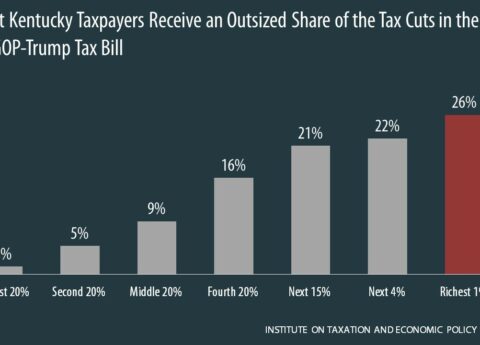

Some Federal Lawmakers Want to Use New Tax Cuts for the Wealthy as Cause to Undermine Basic Supports for Kentucky Families

The tax bill Congress passed yesterday was the first in a two-step plan to cut taxes for the wealthy and...

Kentucky Center for Economic Policy

Research That Works for Kentucky