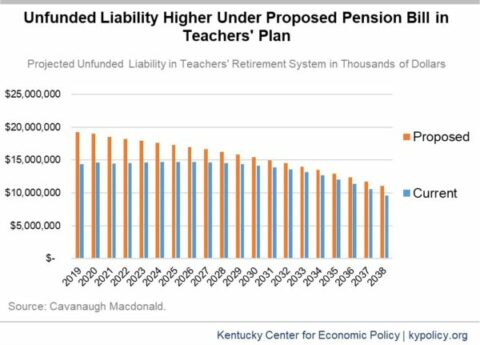

Analysis Shows Pension Bill Adds Huge New Costs for Teachers’ Plan

A new analysis of the proposed pension bill by the actuary for the Teachers' Retirement System (TRS) shows huge new costs...

Kentucky Center for Economic Policy

Research That Works for Kentucky