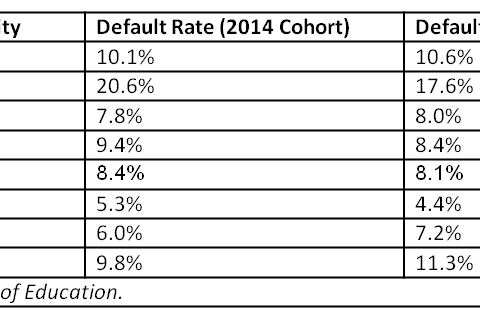

Kentucky again ranks among the worst states for rates of student loan default, according to new data released by the U.S. Department of Education. This latest data is yet another...

Calls to end Kentucky's defined benefit (DB) public pension plans often refer to the move away from DB plans in the private sector and suggest the public sector should follow...

The latest attempt to repeal the Affordable Care Act (ACA) is known as Cassidy-Graham, and it very well may be the greatest threat to Kentucky’s health care we’ve seen. The...

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok