Click here to view as PDF. The just concluded 2017 legislative session was not a budget session. However, the General Assembly passed a number of bills that will have an...

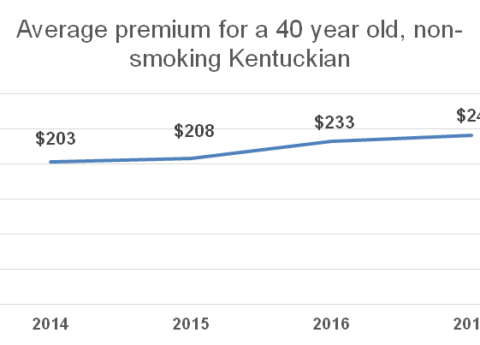

Far from collapsing, the health insurance exchanges set up by the Affordable Care Act (ACA) are a way many Kentuckians are now able to buy health insurance. It will be...

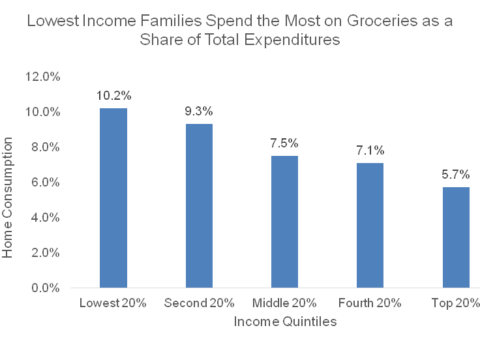

Click to view as a PDF. Governor Bevin has said he will propose tax reform in a special session this year that will move Kentucky toward a “consumption-based” tax system...

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok