With the 2017 Kentucky General Assembly in the books, Governor Bevin and the legislature will now turn their attention to a possible special session later this year that will focus...

The 2017 General Assembly has ended, but the full impact on workers of several harmful bills passed during the session will play out for years to come. In the very...

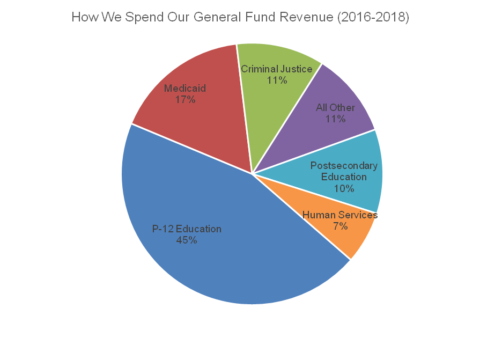

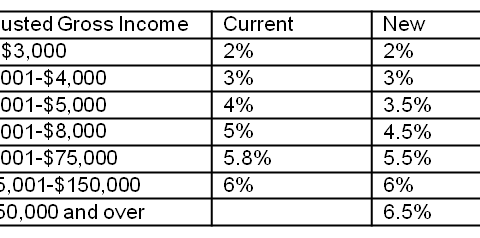

Across the commonwealth, Kentuckians are filing their taxes this week; and many are wondering if and how the Governor’s intention to do tax reform this year will impact what they...

Click here to view as a PDF. Though the details remain unknown, Governor Bevin has described the kind of tax reform he’ll introduce in a special session this year as...

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok