To read KCEP’s submitted comments on the rule, click here.

The Consumer Financial Protection Bureau (CFPB) released its long awaited proposed rule to reign in many abusive practices of payday lenders nationwide. In Kentucky, this would impact roughly 200,000 mostly low-income payday lending customers.

While Kentucky law limits annual interest rates on financial products to a maximum of 36 percent, payday lenders are exempt, and can issue unsecured loans for $15 per $100 borrowed, for up to $500, often for a 2-week term. Borrowers are not allowed to have more than 2 loans out at any given point in time, but this still makes it possible for a single borrower to take out 52 loans a year – which, when annualized, results in a 390 percent APR. In fact, the average borrower pays $591 in interest and fees for an average principal of $341 according to the annual report by Veritec, the company that maintains the Payday Lending database for the Kentucky Department of Financial Institutions.

The real danger of payday loans is the rollover encouraged by the industry. When a borrower takes out a loan, they give the lender access to their account, either electronically or through a post-dated check. At the end of the loan period, the lender draws the principal and interest from that account, which often leads the borrower to take out another loan to fill the financial hole. This cycle then repeats itself to the extent that the average Kentucky payday loan customers takes out 10.6 loans and is indebted over 200 days a year. Over 95 percent of all payday loans in Kentucky go to customers that take out 4 or more loans per year, while only 1 percent of payday loans go to single-use borrowers. This cycle is often referred to as the ‘debt trap.’

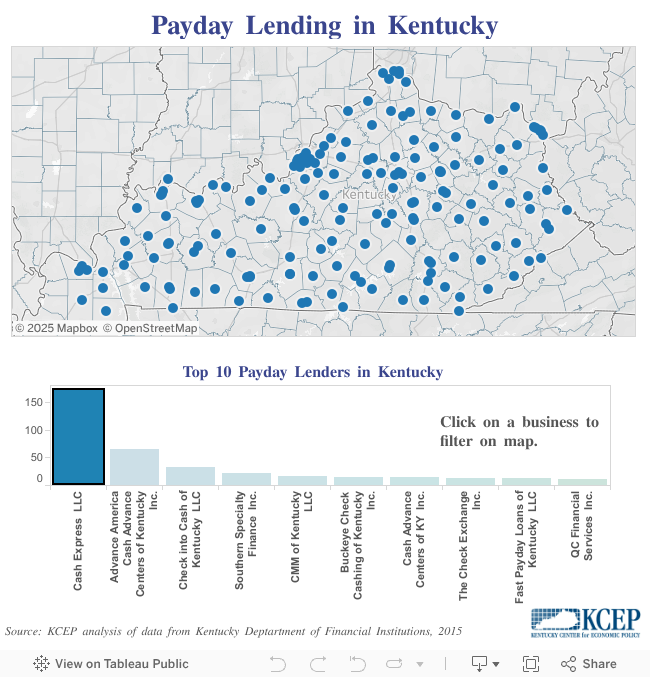

There are 537 active “Check Cashing” licenses registered with the Department of Financial Institutions in Kentucky, most of which offer some kind of small-dollar, short-term, unsecured loans like payday loans. Cash Express, the largest payday lending company in Kentucky, operates 172 stores in almost every county in the state, and is headquartered in Tennessee.

While the CFPB cannot regulate interest rates, the proposed rule does seek to limit the so-called debt trap in two main ways:

- Payday lenders would have to prove that the borrower has the ability to repay the loan while still being able to afford major financial obligations and basic living expenses, without needing to re-borrow.

- Payday lenders can issue loans without determining a borrower’s ability to repay if their loan meets certain requirements:

- Lenders would be limited to offering just 3 loans in quick succession, where the first loan is no more than $500, the 2nd loan is 2/3 the amount of the 1st, and the 3rd loan is 1/3 the amount of the 1st;

- Lenders would only be able to offer a total of 6 loans or keep a borrower in debt for a maximum of 90 days total in any given 12-month period;

- And lenders would not be allowed to take vehicle security on loans (often referred to as title loans, which are regulated in Kentucky beyond what the CFPB is proposing).

The final rule is expected to be months away, after an extensive public-comment period and further review. During that time, further measures to strengthen the rule like combining the ability to repay requirement with the loan restrictions should be included. The rule as it stands would be a step toward meaningful financial protections for the low-income customers, but it should be made stronger.

Advocacy for payday lending reform in Kentucky has been spearheaded by a broad coalition of 88 faith-based and non-profit organizations, known as the Kentucky Coalition for Responsible Lending. The coalition has been pursuing a 36 percent usury limit to payday loans, which has been introduced in the General Assembly several times over the last 10 years. While the CFPB cannot cap interest rates, the General Assembly can and should as it is the gold standard for safe lending practices. Additionally, as the final rule takes effect, Kentucky lawmakers should remain vigilant for new predatory lending products that seek to work around state and federal regulations.