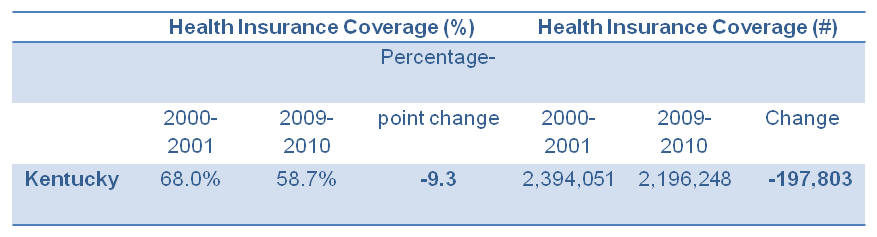

According to a new report from the Economic Policy Institute (EPI), 200,000 fewer non-elderly Kentuckians had health insurance through an employer in 2010 than in 2000. The report finds that employer-sponsored insurance declined 9.3 percentage points over that period. Only 58.7 percent of Kentuckians under age 65 had this type of coverage in 2010.

The EPI report describes how, at the national level, those with lower levels of education and lower wages are less likely to have health insurance through an employer—or be insured at all.1 According to the report, “Nearly one-third of all workers in the lowest 40 percent of the wage distribution are uninsured, compared with less than one-eleventh of workers in the top 40 percent.” The report also documents racial disparities in health insurance coverage. In 2010, non-Hispanic whites experienced rates of coverage through an employer 71 percent higher than those of Hispanics and 48 percent higher than those of blacks.2

The decline in employer-sponsored health insurance is not just because of the bad economy of the last few years. Of those working, 8.5 percentage points fewer had employer-sponsored insurance in 2010 than in 2000. And employer-sponsored coverage in Kentucky declined 7.3 percentage points just between 2000 and 2007—before the most recent recession. The erosion of coverage is evidence of the continued inadequacies of our employer-based health insurance system in the face of rising health care costs.

While Medicaid continues to provide coverage for the very poor—and enrollment is growing rapidly—most working families without employer-sponsored insurance currently do not qualify for Medicaid yet cannot afford individual insurance plans. More than 826,400 adults currently participate in Kentucky’s Medicaid program, and enrollment is expected to continue growing at an estimated 1,550 new members a month. 3 However, current state Medicaid guidelines disqualify all but the very poor; for instance, for a family of four, monthly income after deductions can be no more than $383.4

Should it survive court challenges, health reform will help address this gap and provide affordable health insurance for working families. The Affordable Care Act will expand Medicaid to qualify those with incomes up to 133 percent of the poverty level and will provide health insurance options for individuals, families and small businesses through the operation of health care exchanges. 5 As a result of full implementation of the legislation in 2014, the share of nonelderly Kentuckians who are uninsured is expected to decrease 13.1 percentage points—from 20 percent before reform to 6.8 percent after. Only six other states are expected to see a more significant decrease.6

Source: Economic Policy Institute Analysis of US Census Bureau Data

- Elise Gould, “A Decade of Declines in Employer-Sponsored Health Insurance Coverage,” Economic Policy Institute, February 23, 2012, http://www.epi.org/publication/bp337-employer-sponsored-health-insurance/. ↩

- State-level analyses were not provided. ↩

- Department for Medicaid Services, “Biennial Budget Overview 2013-2014,” presentation to the House Budget Review Subcommittee on Human Resources, February 1, 2012. ↩

- Kentucky Department of Health and Family Services, http://chfs.ky.gov/dms/apply.htm. Retrieved February 17, 2012. ↩

- Under the Affordable Care Act, Kentucky Medicaid would see approximately 300,000 newly enrolled non-elderly adults, and 306,000 non-elderly adults are predicted to receive coverage through nongroup healthcare exchanges. Matthew Buettgens, John Holahan, and Caitlin Carroll. “Health Reform Across the States: Increased Insurance Coverage and Federal Spending on the Exchanges and Medicaid,” Urban Institute, March 2011, http://www.urban.org/UploadedPDF/412310-Health-Reform-Across-the-States.pdf. ↩

- Matthew Buettgens, John Holahan, and Caitlin Carroll. “Health Reform Across the States.” ↩