For the nearly 100,000 Kentuckians who signed up for plans on kynect this year, the state’s health insurance marketplace, premium costs are on track to skyrocket at the end of this year. This hike is due to Congress failing to extend existing subsidies on marketplace plans, which have lowered costs since 2021 and are set to expire, and because of changes made to marketplace plans through the One Big Beautiful Bill Act (OBBBA). Combined, these two policy decisions will lead to subsidized premiums more than doubling in many cases, and have already led to rattled insurance carriers increasing the unsubsidized cost of insurance by up to 37% for Kentuckians seeking coverage — more than 10 times higher than in recent years. As many as 18,000 Kentuckians would have to leave the marketplace as a result of the higher costs and most of them would become uninsured.

Because both causes of this spike in health care costs are due to Congressional decisions, it is up to Congress to work quickly to address the problem before open enrollment for the 2026 plan year begins November 1. As Congress prepares to take action on the federal budget for the upcoming fiscal year that starts October 1, lawmakers should prioritize keeping the marketplace coverage option affordable, particularly given the seismic cuts to Medicaid passed earlier this year that will take health care away from more than 200,000 Kentuckians.

Congress is raising health insurance costs in two different ways

The first way in which Congress is set to raise health care costs is by allowing recently improved subsidies to expire on December 31, which will affect open enrollment at the end of this year.

Since 2014, for households whose income is too high to qualify for Medicaid but don’t receive health insurance elsewhere (like at work), kynect offers income-based, federally-funded subsidies that reduce the cost of health coverage. Health insurance companies set rates based on county, age and smoking status, and then the federal government provides advanced premium tax credits (APTCs) that offset a portion of that cost. In 2021, the American Rescue Plan Act improved those subsidies in several ways, including:

- Lowering the caps on premium contributions for people of all income levels;

- Allowing people with incomes between 100% and 150% of the poverty level to pay $0 in premiums for “benchmark” silver-level plans; and

- Extending eligibility for APTCs to people with incomes above 400% of the poverty level if their benchmark premiums would exceed 8.5% of household income.

The enhanced subsidies came at a pivotal time, when many were no longer eligible for pandemic-era Medicaid coverage. As a result, many of those who lost Medicaid coverage were able to afford a marketplace plan, with enrollment jumping from 74,882 in 2024 to 97,374 this year. While the average unsubsidized plan cost $601 per-month, the enhanced subsidies resulted in an average of $119 out-of-pocket premiums per-month for the 83,518 enrollees who received them, and many had $0 per-month plans.

The second way Congress is raising the cost of kynect’s health insurance plans is through new barriers erected through the OBBBA. As summarized by the Urban Institute, the key provisions include:

- Shortening annual open enrollment periods, including among state-based marketplaces, which currently have the flexibility to set the periods themselves;

- Requiring additional paperwork to verify income if an Internal Revenue Service (IRS) data match cannot provide income data, or returns income below 100% of the federal poverty level (FPL);

- Reducing the applicable percentages of income for PTCs, leading to higher out-of-pocket premiums;

- Eliminating automatic reenrollment with APTC, which 60% of Kentucky enrollees used in 2025;

- Ending the special enrollment period for people with incomes below 150% of FPL and imposing additional verification requirements for other special enrollment periods;

- Disqualifying consumers from APTCs if, for a single past year, they received APTCs and the IRS cannot confirm that they filed a tax return and completed the reconciliation process;

- Requiring consumers who are automatically reenrolled in the marketplace with no premium to pay $5 per month until they come back to the marketplace and establish their eligibility;

- Greatly narrowing the eligibility of lawfully present immigrants for marketplace PTCs; and

- Eliminating provisional eligibility for APTC while eligibility is being verified.

The Congressional Budget Office estimated that the OBBBA will result in 10.9 million Americans losing healthcare nationally and that in over a third of cases (3.6 million) it would be due to the changes impacting marketplace plans. It further estimated that 4.2 million more would lose health care due to failure to extend the enhanced APTCs.

The result of the failure to extend the improved subsidies and the introduction of these new barriers to coverage has already led Kentucky insurers to increase their rate changes to the plans they offer on kynect from a range of 9.9%-24% before the passage of OBBBA to 15.1%-37% following OBBBA. These increases are due to the uncertainty of the number, health, and cost to cover those who remain in marketplace plans.

In addition to these increases in the base cost of insurance, the reduced value of the APTCs — as well as the reinstated cap on who can receive them — will further increase the out-of-pocket costs. For example, a family in Berea earning $50,000 per-year with two 45-year-old parents and a 14-year-old child will see their monthly premium rise from $63 per-month to $250 per-month. Or a 60-year-old small business owner in Christian County earning $62,700 per year would see her monthly premium spike from $444 to $933. In essence, Congress has shifted costs from the federal government to workers and their families.

To estimate premium increases resulting from the expiring APTCs by zip code, household composition, and smoking status, Kaiser Family Foundation has created an interactive tool here.

Health care cost spikes will primarily harm working families and those with health conditions

The marketplace was designed to fill the “coverage gap” beyond the lowest-income families covered by Medicaid (up to 138% of the poverty level) and those who receive coverage at work, through the Veterans Administration or through Medicare. Adults in these families include many employees who earn too much for Medicaid but are not offered affordable coverage at work or any employer-sponsored coverage at all. The largest group of adults covered by the marketplace are small business owners and self-employed individuals, who account for half the marketplace-covered adults.

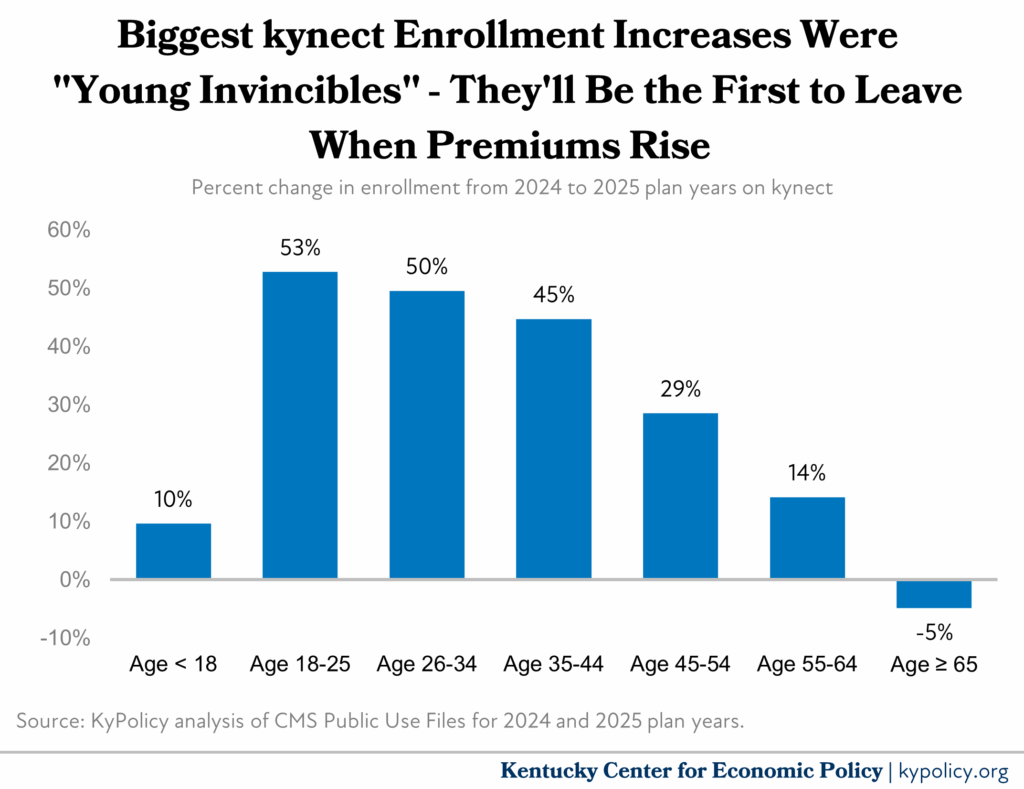

In Kentucky, the enhanced subsidies and longstanding enrollment rules have led toa much stabler, more robust marketplace. Last year, there were four insurance carriers offering plans, rate increases were low, and enrollment was at a near-record high. Perhaps the most important factor in keeping costs down last year was the significant jump in the number of young people in good health, which helps to balance out the “risk pool” for insurers by allowing the premiums of healthier individuals to help cover the cost of care for those with more health problems, thereby keeping premium costs stable for everyone. These younger enrollees are often called “Young Invincibles,” and their enrollment in kynect plans increased by thousands, with 53% more of the youngest adults signing up in 2025 than in 2024.

But because these individuals tend to have fewer health care needs, they are often the first to drop coverage when premiums increase, which destabilizes the market and will further increase premiums in future years. Ultimately, their exit will make health coverage unaffordable or completely out of reach for those struggling with a medical condition and therefore need coverage the most. It also puts these young people at risk of enormous medical bills if they face an unexpected accident or illness.

Congress should act fast to prevent coverage costs from skyrocketing

The only way to prevent health costs from spiking is funding from Congress. Not extending the enhanced subsides and enacting the new barriers in OBBBA will cost five million Americans (including 13,000 Kentuckians) their health care. In Kentucky, this would amount to a 6% increase in our uninsured population, and almost certainly would have secondary costs to the state and federal governments, as well as further straining an already fragile health care system.

Congress is currently contemplating the next year’s budget which begins October 1, and open enrollment for the 2026 plan year doesn’t start until November 1. There is still time to extend these broadly popular and vital health care options, and Kentucky’s federal delegation should prioritize doing so.

Photo: Former Gov. Steve Beshear on Flickr