On July 25, the extra $600 per week in unemployment benefits known as Federal Pandemic Unemployment Compensation (PUC) expired for Kentuckians receiving jobless benefits, and the pain of that lost...

As with states, local governments in Kentucky and nationwide need significant federal relief if they are to continue providing crucial front line and community services through the COVID-19 pandemic. Measures...

As the COVID-19 pandemic leads to layoffs and school closures, and as more people are staying at home to reduce the risk of infection, having enough food will be an...

Amid the spread of COVID-19 and resulting business closures and layoffs, a recession is under way and could be particularly harmful in Kentucky due to the state’s failure to adequately...

The budget passed by the House mostly avoids another round of damaging cuts to programs and services that have been common since the Great Recession (with a few important exceptions,...

The House budget plan includes many of the same priorities that the governor proposed, but contains a different emphasis in a variety of areas. Compared to the governor’s budget, the...

All Kentucky children – living in poor and wealthy districts, black, brown and white, whose parents didn’t finish high school and that have advanced degrees – deserve a high-quality education...

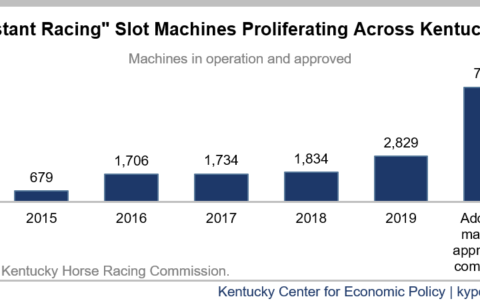

Betting using instant wagering machines, which resemble and operate similar to slot machines, has exploded across Kentucky and thousands more machines will come online in the near future. Yet the...

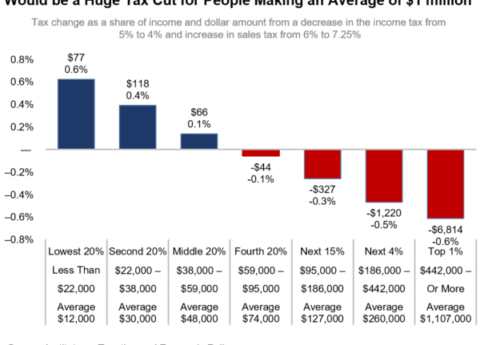

In interviews leading up to the 2020 session, legislative leaders have expressed their desire to continue down the path of reducing income taxes and paying for the reductions by relying...

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok