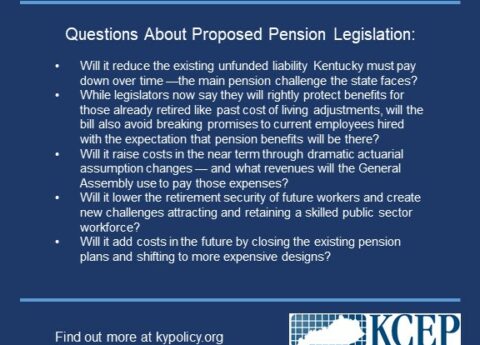

Pension Legislation Should Solve Real Problems and Avoid Harmful Consequences

Legislative leaders say they will soon share a framework for potential pension legislation the General Assembly will consider in a...

Kentucky Center for Economic Policy

Research That Works for Kentucky