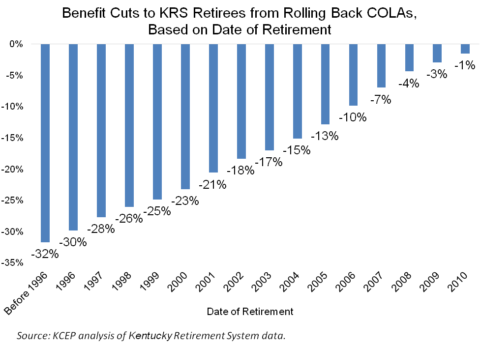

The Bevin administration's consultant recommends a massive cut to many retirees' incomes by rolling back past cost of living adjustments (COLAs) — a proposal that could reduce pension checks by...

The final report from the state’s pension consultant PFM uses exaggerated claims about the condition of all of the state's pension plans to justify harsh and ultimately counterproductive cuts to...

In January, Gov. Bevin announced he would call a special session this year on pensions and tax reform. At the time, he said the issues must go together and rightly...

The recent U.S. House budget resolution would slash the Pell Grant program by $75 billion over the next decade, cutting the maximum grant by $1,060 or 18 percent. Pell Grants...

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok