Four years after Kansas began its “real live experiment” cutting taxes for wealthy and powerful interests, the damaging consequences – including a deeply underfunded education system, college tuition hikes, crumbling...

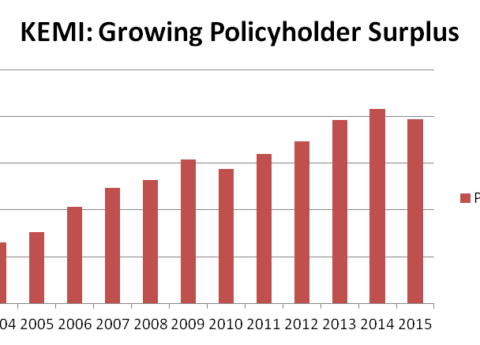

To view this as a PDF, click here. State legislation enacted in recent decades has limited workers’ compensation benefits in Kentucky. As a result, workers’ compensation insurers have benefited, which...

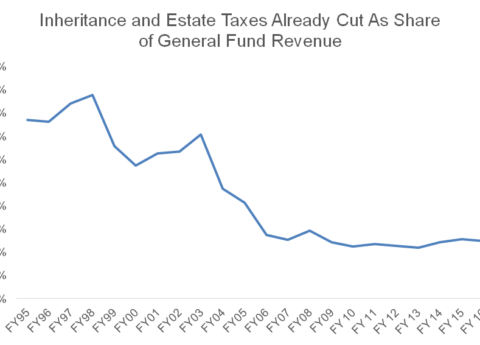

To view this brief in PDF format, click here. Since 1906, Kentucky has relied on the inheritance tax to help pay for the good schools, infrastructure and other investments that...

Tuesday's election means total Republican control of state government with the party gaining a majority in the House for the first time in 95 years. Now the governor and legislative...

Last week Kentucky’s Public Advocate Ed Monahan testified to the Interim Joint Committee on Judiciary that the state needs to reform its Persistent Felony Offender (PFO) laws. This is also...

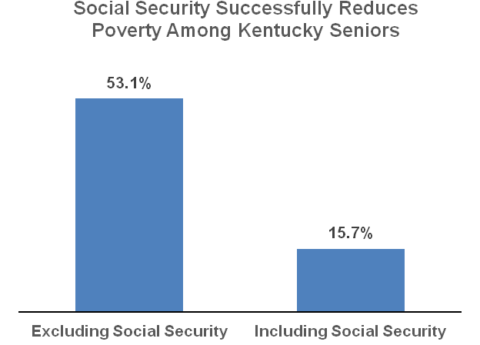

Social Security helps nearly a million Kentuckians make ends meet, cuts senior poverty dramatically and supports local economies by ensuring more people have money in their pockets to spend, as...

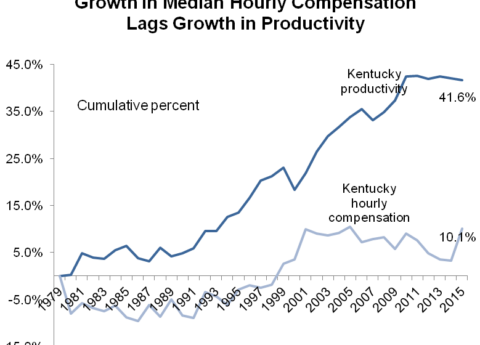

Wages for Kentucky workers finally grew last year, suggesting both a tightening labor market and pointing to strong recent growth in manufacturing and health care jobs, among other industries. But...

"Report: State's School Budget Cuts Nation's Third-Worst" by Keith Lawrence

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok