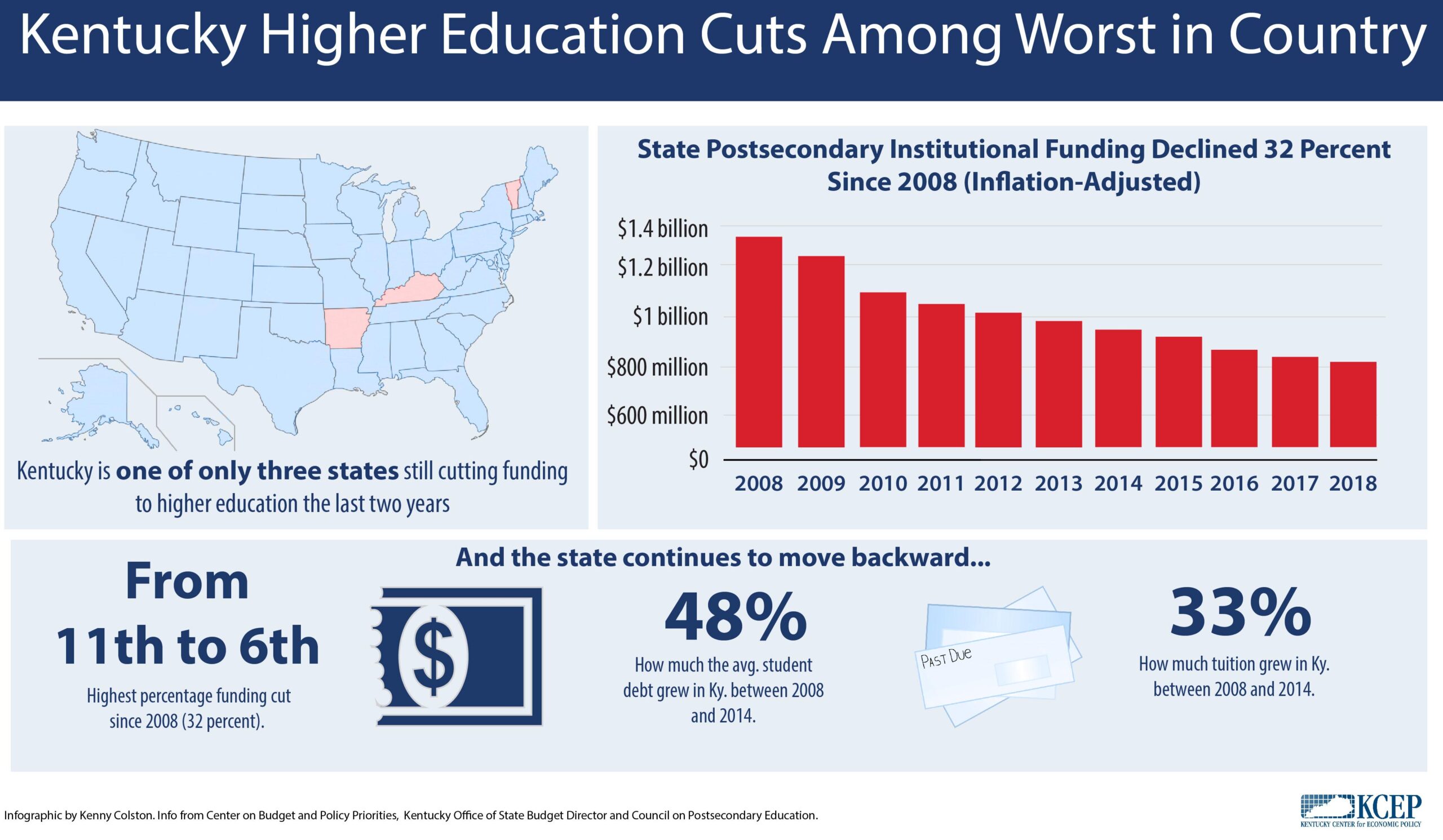

Kentucky is continuing its tumble to the bottom as one of the worst states in funding cuts to higher education, a new report from the Center for Budget and Policy...

To read KCEP's submitted comments on the rule, click here. The Consumer Financial Protection Bureau (CFPB) released its long awaited proposed rule to reign in many abusive practices of payday...

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok