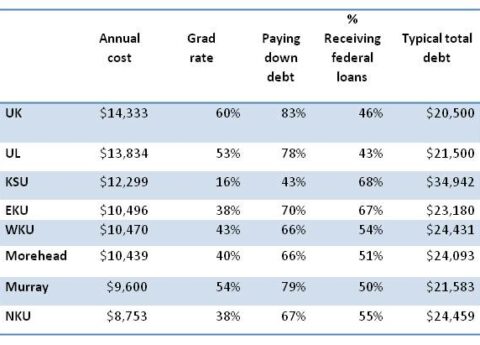

New Data Shows Kentuckians with Third-Highest Student Loan Default Rate Among States

New data shows that Kentuckians leaving college with student loan debt have among the highest default rates in the country,...

Kentucky Center for Economic Policy

Research That Works for Kentucky